One day a blond who had no past experience in horseback riding, decided to try.

She mounted the horse, and it started to gallop, the horse kept going faster, and faster. The blond lost control and started to slide down the side of the horse. So she made a grab for the horse's tail, but couldn't get a good grip.

She then reached for the horse's mane, still she couldn't get a good grip. Now she was at the mercy of the horse's pounding hooves.

Fortunately, Dave the Wal-Mart manager, came and unplugged the horse...

Saturday, December 25, 2010

Wednesday, December 22, 2010

Mr. Stephen Schwarzman’s lecture at Yale

I really enjoyed listening and watching Mr. Stephen Schwarzman’s lecture at Yale. Mr.Schwarzman discussed many topics such as the nature of private equity, real estate, successful and failed deals, and how the financial crisis occurred and evolved. I have read and heard so much of the financial crises by now, that I thought there was nothing new that I could learn. I was wrong.

I learned from Mr. Schwarzman’s lecture that government policies and laws can lead to unintended negative consequences in our society. Although this was not the main point of his discussion, he did refer to a few government actions that had clear and unintended negative consequences for our society.

The first was the start of the real estate bubble, which began with the US government’s policy to get more people into homes. Although this was a good policy, it wound up turning into a fiasco, with all the unintended consequences to come later. For example, Mr. Schwarzman stated that subprime mortgages at one point were 2-3% of all mortgages; and by the end they had become more than 30%. He also described how 87% of pooled mortgages which were securitized were given AAA ratings. This misled investors into thinking that these securities were safe and could not default. Mr. Schwarzman believes historians will look back at this time and wonder how AAA ratings were given to these securities in the first place. In addition, he wonders how so many investors believed in these ratings and were fooled by them. In my opinion it’s pretty simple; just like there is a fog of war and a fog of panic, there is also the fog of greed.

The second unintended negative consequence came from the passage of the Sarbanes-Oxley law. This law was passed after the Enron scandal and created fair value accounting, also known as FAS 157. Mr. Schwarzman described how FAS 157 forced financial institutions to take losses before defaults actually occurred. These losses, in turn, created a crisis of confidence in financial institutions which eventually morphed into the much bigger financial crisis.

His stories of successful deals, US Steel and Celanese, and unsuccessful ones, an Argentinian cell phone company, were also interesting. One point he stressed was that capital always comes back. Even though there is a credit crunch occurring, he is optimistic that credit and capital will come back. He mentioned the past credit crunches of 1975, 1982, 1987, and 1990-1991.

I also liked his discussion about failure. He stated how he hates failure and when it does occur that he tries to learn from it. Failure can be a blessing in disguise. Mr. Schwarzman is a winner because he does not like to fail. This was worth watching.

I learned from Mr. Schwarzman’s lecture that government policies and laws can lead to unintended negative consequences in our society. Although this was not the main point of his discussion, he did refer to a few government actions that had clear and unintended negative consequences for our society.

The first was the start of the real estate bubble, which began with the US government’s policy to get more people into homes. Although this was a good policy, it wound up turning into a fiasco, with all the unintended consequences to come later. For example, Mr. Schwarzman stated that subprime mortgages at one point were 2-3% of all mortgages; and by the end they had become more than 30%. He also described how 87% of pooled mortgages which were securitized were given AAA ratings. This misled investors into thinking that these securities were safe and could not default. Mr. Schwarzman believes historians will look back at this time and wonder how AAA ratings were given to these securities in the first place. In addition, he wonders how so many investors believed in these ratings and were fooled by them. In my opinion it’s pretty simple; just like there is a fog of war and a fog of panic, there is also the fog of greed.

The second unintended negative consequence came from the passage of the Sarbanes-Oxley law. This law was passed after the Enron scandal and created fair value accounting, also known as FAS 157. Mr. Schwarzman described how FAS 157 forced financial institutions to take losses before defaults actually occurred. These losses, in turn, created a crisis of confidence in financial institutions which eventually morphed into the much bigger financial crisis.

His stories of successful deals, US Steel and Celanese, and unsuccessful ones, an Argentinian cell phone company, were also interesting. One point he stressed was that capital always comes back. Even though there is a credit crunch occurring, he is optimistic that credit and capital will come back. He mentioned the past credit crunches of 1975, 1982, 1987, and 1990-1991.

I also liked his discussion about failure. He stated how he hates failure and when it does occur that he tries to learn from it. Failure can be a blessing in disguise. Mr. Schwarzman is a winner because he does not like to fail. This was worth watching.

Tuesday, December 21, 2010

60 Minutes and The Day of Reckoning

This past Sunday night, “60 Minutes,” the television show, had a segment on the looming financial crisis of local, municipal, and state governments. The analyst who was interviewed, along with Governor Chris Christie of New Jersey, basically said the same thing. The Day of Reckoning is here and will need to be addressed. What does this mean? It means more catastrophic losses and bailouts by the US taxpayer.

According to the analyst, this will begin to occur within the next 12 months. Mr. Christie says that it is already here. This is serious and no one seems to care. For years I have been hearing of unfunded pension liabilities, creative accounting, and budget deficits-yet no one has done anything about it.

The show also stated how Illinois is effectively bankrupt and a deadbeat. Why have we not heard more about these issues? Are we ostriches with our heads in the sand ? Is our government unwilling to talk about this future crisis? I commend “60 Minutes” for this segment, but it makes me nervous. Just like everything else that is happening…

According to the analyst, this will begin to occur within the next 12 months. Mr. Christie says that it is already here. This is serious and no one seems to care. For years I have been hearing of unfunded pension liabilities, creative accounting, and budget deficits-yet no one has done anything about it.

The show also stated how Illinois is effectively bankrupt and a deadbeat. Why have we not heard more about these issues? Are we ostriches with our heads in the sand ? Is our government unwilling to talk about this future crisis? I commend “60 Minutes” for this segment, but it makes me nervous. Just like everything else that is happening…

Friday, December 17, 2010

ZZJoke.com - Joke

A couple of hunters were out in the woods when one of them fell to the ground clutching his chest.

After struggling for a few seconds,he seemed to stop breathing. The other hunter quickly pulls out his cellphone and dials 911.

He gasps to the operator, "My friend is dead! What should I do?"

In a soothing voice, the operator says, "Try to remain calm, sir. I can help you. First, we need to make sure he's dead."

Immediately the operator heard a shot.

The frantic hunter comes back on the line and says, "Okay, now what?"

After struggling for a few seconds,he seemed to stop breathing. The other hunter quickly pulls out his cellphone and dials 911.

He gasps to the operator, "My friend is dead! What should I do?"

In a soothing voice, the operator says, "Try to remain calm, sir. I can help you. First, we need to make sure he's dead."

Immediately the operator heard a shot.

The frantic hunter comes back on the line and says, "Okay, now what?"

Thursday, December 16, 2010

MBA and the Top Business Schools

Here’s a pretty good site that summarizes a typical MBA program. Also, Bloomberg Businessweek has released what it considers the best business schools in the country.

Wednesday, December 15, 2010

Confucius Peace Prize - Nobel - China - Liu

China is very unhappy with this year’s Nobel Peace Prize winner; Mr. Liu Xiaobo. Mr. Liu is serving eleven years in a Chinese prison for supporting political reform, human rights, and an independent judicial system. In response, China has created its own peace prize, the Confucius Peace Prize.

Maybe the Nobel Peace Prize committee is politically motivated, for example, the choice of President Barack Obama was debatable and raised questions. We all can see this as a politically motivated game, but what I find interesting is the list of countries that have now rejected invitations to the Nobel Peace Prize ceremony. The list includes:

China

Afghanistan

Columbia

Cuba

Egypt

Iran

Iraq

Kazakhstan

Morocco

Pakistan

Philippines

Russia

Saudi Arabia

Serbia

Sudan

Tunisia

Ukraine

Venezuela

Vietnam

Here are some themes these countries represent: opposition to the U.S. and its policies, Arabs, natural resources, and non-Western. I’ll let the reader decide what they think of this, but it does make one wonder why they are not going.

Maybe the Nobel Peace Prize committee is politically motivated, for example, the choice of President Barack Obama was debatable and raised questions. We all can see this as a politically motivated game, but what I find interesting is the list of countries that have now rejected invitations to the Nobel Peace Prize ceremony. The list includes:

China

Afghanistan

Columbia

Cuba

Egypt

Iran

Iraq

Kazakhstan

Morocco

Pakistan

Philippines

Russia

Saudi Arabia

Serbia

Sudan

Tunisia

Ukraine

Venezuela

Vietnam

Here are some themes these countries represent: opposition to the U.S. and its policies, Arabs, natural resources, and non-Western. I’ll let the reader decide what they think of this, but it does make one wonder why they are not going.

Tuesday, December 14, 2010

Yes, You Can Time the Market ! - Ben Stein - Phil DeMuth

I have just completed reading the book Yes, You Can Time the Market !, by Mr. Ben Stein and Mr. Phil DeMuth. The book is a well-written, no nonsense book, which gives practical and easy advice to follow for those who have a long term investment horizon. The authors have done their homework and they also discuss other academic studies which support their ideas. The authors make no claim that market timing can be done in the short run. If, however, you have a long term investment horizon (15-20 years), then buying when the market is “low” will generate better returns over other investment strategies.

So, you may ask, what is low? The authors look at a variety of criteria, such as market price, PE ratios, dividend yield, price to book, Tobin’s Q, price to cash flow, etc. In general, they argue that returns for any 5, 10, 15, 20 year period were higher when investors entered the market when it was trading better than the respective long term average of 15 years. For example, buying the SP500 when it was trading below its 15 year moving average price, was generally a good time to enter the market.

The authors are not ignorant that many times you may be sitting on the sideline feeling foolish as markets head to the moon, but they believe you will be rewarded over time because:

“Unlike other stock market anomalies, which disappear the moment they are pointed out, buying low promises to endure. This is because the extra returns it delivers do not come free. Rather they are a payment for assuming the psychological burden of buying stocks when everyone says the sky is falling, and demurring when Wall Street is having a feeding frenzy.”

The authors also believe that markets regress to the mean. This is why groups of stocks with high PE’s tend to underperform in future years, compared to groups of stocks with low PE’s, which outperform going forward. Another example of regressing to the mean was discussed in the performance of stock prices. Stocks that have outperformed (underperformed) over the past few years tend to underperform (outperform) in the future.

This is a good book to read for those who believe in investing for the long run. I enjoyed it and would recommend it.

The authors summarize their work in the following paragraph:

“The point of this book-so simple that a child can grasp it, yet so elusive that your broker will never get it-is that you are better off buying cheap.”

So, you may ask, what is low? The authors look at a variety of criteria, such as market price, PE ratios, dividend yield, price to book, Tobin’s Q, price to cash flow, etc. In general, they argue that returns for any 5, 10, 15, 20 year period were higher when investors entered the market when it was trading better than the respective long term average of 15 years. For example, buying the SP500 when it was trading below its 15 year moving average price, was generally a good time to enter the market.

The authors are not ignorant that many times you may be sitting on the sideline feeling foolish as markets head to the moon, but they believe you will be rewarded over time because:

“Unlike other stock market anomalies, which disappear the moment they are pointed out, buying low promises to endure. This is because the extra returns it delivers do not come free. Rather they are a payment for assuming the psychological burden of buying stocks when everyone says the sky is falling, and demurring when Wall Street is having a feeding frenzy.”

The authors also believe that markets regress to the mean. This is why groups of stocks with high PE’s tend to underperform in future years, compared to groups of stocks with low PE’s, which outperform going forward. Another example of regressing to the mean was discussed in the performance of stock prices. Stocks that have outperformed (underperformed) over the past few years tend to underperform (outperform) in the future.

This is a good book to read for those who believe in investing for the long run. I enjoyed it and would recommend it.

The authors summarize their work in the following paragraph:

“The point of this book-so simple that a child can grasp it, yet so elusive that your broker will never get it-is that you are better off buying cheap.”

Monday, December 13, 2010

Mr. David Swensen's Lecture - Yale - Shiller

I have always known about the excellent returns generated by the Yale endowment, but have never dug deeper to find out who is responsible for those returns. Since reading Mr. Biggs book, Hedgehogging, I have come to find out the man responsible is Mr. David Swensen. I recently watched a great lecture by Mr. Swensen and would like to share some of the main concepts he discussed.

Mr. Swensen begins his lecture by stating that when he came to Yale he decided to study what other institutions were doing at that time. He found that most institutions were allocating their funds, 50%-40%-10%; 50% US stocks, 40% US Bonds, and 10% cash or other. Mr. Swensen felt that this was inappropriate, and began to change the way Yale invested its endowment money.

Given some academic results of studies done by Mr. Ibbotson, Mr. Swensen decided that equities were the place to be in the long run, given their superior long term returns compared to other alternative asset classes. Mr. Swensen also began to look for investments in alternative asset classes. It was very interesting how he decided on where he should allocate most of his time and effort in search of higher risk-adjusted returns. Mr. Swensen decided that inefficient markets would offer better opportunities and could generate market beating returns. The way he determined this was by looking at long run returns of managers within various asset classes, and what the returns were of the top percentile compared to the bottom percentile within each category. He then also looked at the dispersion of those returns:

Bonds .5%

Large Cap Equities 2%

Small Cap Equities 4.7%

Hedge funds 7.1%

Real estate 9.3%

LBO’s 13.7%

Venture Capital 43.2%

It became clear to him that spending more time in the areas where the dispersion was greatest would pinpoint inefficiently priced markets and better investment opportunities. He stated that there was very little reason to spend a lot of time looking for managers in the bond market, where prices are generally mathematically calculated and pricing is very efficient, compared to other types of markets.

Mr. Swenson discussed three large topics in his lecture; asset allocation, market timing, and security selection. He concluded that asset allocation is the number one driver of returns. He discouraged market timing, and he felt that the system is not a zero sum game. Excessive fees charged by hedge funds, commissions, and consultant fees, have turned a zero sum game into a negative sum game.

Mr. Swensen also warned the students to be very careful when evaluating historical performance results. He stressed that data can be skewed by survivorship bias and back-fill bias. Survivorship bias removes the bad performance of managers who have folded and back-fill bias adds in good performance of managers.

At the time of the lecture the Yale endowment was allocated:

11% US Stocks

15% Foreign stocks

4% Bonds

23% Hedge Funds

28% Timber, Oil and gas, real estate

19% Private equity, LBO’s, Venture Capital

This is an excellent lecture and I highly recommend watching it. LINK Mr. Swensen’s long term performance has been exceptional. He did it by becoming equity-oriented, finding great managers who did well in efficiently priced markets, by changing the asset allocation of the total portfolio, and by diversifying the risks. Really quite simple...)

Mr. Swensen begins his lecture by stating that when he came to Yale he decided to study what other institutions were doing at that time. He found that most institutions were allocating their funds, 50%-40%-10%; 50% US stocks, 40% US Bonds, and 10% cash or other. Mr. Swensen felt that this was inappropriate, and began to change the way Yale invested its endowment money.

Given some academic results of studies done by Mr. Ibbotson, Mr. Swensen decided that equities were the place to be in the long run, given their superior long term returns compared to other alternative asset classes. Mr. Swensen also began to look for investments in alternative asset classes. It was very interesting how he decided on where he should allocate most of his time and effort in search of higher risk-adjusted returns. Mr. Swensen decided that inefficient markets would offer better opportunities and could generate market beating returns. The way he determined this was by looking at long run returns of managers within various asset classes, and what the returns were of the top percentile compared to the bottom percentile within each category. He then also looked at the dispersion of those returns:

Bonds .5%

Large Cap Equities 2%

Small Cap Equities 4.7%

Hedge funds 7.1%

Real estate 9.3%

LBO’s 13.7%

Venture Capital 43.2%

It became clear to him that spending more time in the areas where the dispersion was greatest would pinpoint inefficiently priced markets and better investment opportunities. He stated that there was very little reason to spend a lot of time looking for managers in the bond market, where prices are generally mathematically calculated and pricing is very efficient, compared to other types of markets.

Mr. Swenson discussed three large topics in his lecture; asset allocation, market timing, and security selection. He concluded that asset allocation is the number one driver of returns. He discouraged market timing, and he felt that the system is not a zero sum game. Excessive fees charged by hedge funds, commissions, and consultant fees, have turned a zero sum game into a negative sum game.

Mr. Swensen also warned the students to be very careful when evaluating historical performance results. He stressed that data can be skewed by survivorship bias and back-fill bias. Survivorship bias removes the bad performance of managers who have folded and back-fill bias adds in good performance of managers.

At the time of the lecture the Yale endowment was allocated:

11% US Stocks

15% Foreign stocks

4% Bonds

23% Hedge Funds

28% Timber, Oil and gas, real estate

19% Private equity, LBO’s, Venture Capital

This is an excellent lecture and I highly recommend watching it. LINK Mr. Swensen’s long term performance has been exceptional. He did it by becoming equity-oriented, finding great managers who did well in efficiently priced markets, by changing the asset allocation of the total portfolio, and by diversifying the risks. Really quite simple...)

Saturday, December 11, 2010

From ZZJoke.com

Dear Abby,

My husband is not happy with my mood swings.

The other day, he bought me a mood ring so he would be able to monitor my moods.

When I'm in a good mood it turns green.

When I'm in a bad mood it leaves a big red mark on his forehead.

Maybe next time he'll buy me a diamond.

Sincerely,

Moody in Buffalo

My husband is not happy with my mood swings.

The other day, he bought me a mood ring so he would be able to monitor my moods.

When I'm in a good mood it turns green.

When I'm in a bad mood it leaves a big red mark on his forehead.

Maybe next time he'll buy me a diamond.

Sincerely,

Moody in Buffalo

Friday, December 10, 2010

Stoicism and Trading - Stoics

Stoicism was a philosophy towards life that evolved in ancient Greece. Stoicism was founded by Zeno of Citium around 300 B.C. and was later popularized by Chrysippus, Seneca, Epictetus, and Marcus Aurelius.

The philosophy that stoics lived by was to be indifferent to pain or pleasure. They were not easily excited or upset. In a way they were like Zen Buddhists who follow “The Way,” the Tao, by taking the middle road. Stoic philosophy can be useful for traders. Don’t get too thrilled when you hit winners, don’t get too bummed out when you have losses, don’t get really bummed out when you are in long, painful drawdowns, and keeping your head level is philosophically stoic.

I consider myself emotional and sensitive. I like to live life. I emotionally exaggerate life’s highs and lows. It is in my nature. As I am becoming and getting older, I get better in managing my feelings, thoughts, and emotions. It is not easy, and I am sure some people are better in managing their states than others. Nonetheless, we all need to do it. Knowing what I am like as a person helped me in deciding how I would approach trading. I realized pretty quickly that discretionary trading was too difficult and emotional for me. System trading, however, gave me some “emotional separation” from the market. It also helped me be more stoic about my trading performance. Being a systematic trader helps me better manage my emotional states.

Perhaps we cannot live stoically in all aspects of our lives, but we can, however, benefit from its ideas in our trading.

The philosophy that stoics lived by was to be indifferent to pain or pleasure. They were not easily excited or upset. In a way they were like Zen Buddhists who follow “The Way,” the Tao, by taking the middle road. Stoic philosophy can be useful for traders. Don’t get too thrilled when you hit winners, don’t get too bummed out when you have losses, don’t get really bummed out when you are in long, painful drawdowns, and keeping your head level is philosophically stoic.

I consider myself emotional and sensitive. I like to live life. I emotionally exaggerate life’s highs and lows. It is in my nature. As I am becoming and getting older, I get better in managing my feelings, thoughts, and emotions. It is not easy, and I am sure some people are better in managing their states than others. Nonetheless, we all need to do it. Knowing what I am like as a person helped me in deciding how I would approach trading. I realized pretty quickly that discretionary trading was too difficult and emotional for me. System trading, however, gave me some “emotional separation” from the market. It also helped me be more stoic about my trading performance. Being a systematic trader helps me better manage my emotional states.

Perhaps we cannot live stoically in all aspects of our lives, but we can, however, benefit from its ideas in our trading.

Thursday, December 9, 2010

Mr. Taleb and Mr. Mandelbrot

Here is a gentleman that is fighting ingrained thoughts, the status quo, and money interests. Mr. Taleb is challenging fundamental concepts that are being used by bankers and financiers. There really is no credible theory to replace what has been used and established on Wall Street over many years. He does mention in this video that VAR (Value at Risk) analysis should be immediately discarded. The question I have is what replaces it? No bank or risk manager can go out there today and justify what they are doing, because there is no “standard model” that they can stand on.

I agree with Mr. Taleb’s views, but throwing out old theories and replacing them with theories that use power laws, etc. is what Mr. Taleb argues for in his books. It’s going to take a long time to change the way things are done. In fact, what is upsetting is that it seems to me that the bankers and financiers have “won.” Nothing has changed and the system is more fragile than ever. Maybe the whole thing just has to implode before things change. I hope not, but it sure feels like that is the way things are moving.

What can we say about Benoit Mandelbrot? He is a visionary. His insights have been brushed aside by the establishment, but someday, if not already, he will eventually be proven right.

I agree with Mr. Taleb’s views, but throwing out old theories and replacing them with theories that use power laws, etc. is what Mr. Taleb argues for in his books. It’s going to take a long time to change the way things are done. In fact, what is upsetting is that it seems to me that the bankers and financiers have “won.” Nothing has changed and the system is more fragile than ever. Maybe the whole thing just has to implode before things change. I hope not, but it sure feels like that is the way things are moving.

What can we say about Benoit Mandelbrot? He is a visionary. His insights have been brushed aside by the establishment, but someday, if not already, he will eventually be proven right.

Wednesday, December 8, 2010

Mr. Warren Buffett’s two rules for making money

Mr. Warren Buffett has been quoted as saying the first rule of making money is not to lose money. The second rule is to remember the first rule.

This is a simple philosophy that is difficult to do. The point is that an investor cannot dig a hole in their capital. Preserving capital, limiting loss, and having a disciplined money management approach are some of the keys to successful investing and trading.

This is a simple philosophy that is difficult to do. The point is that an investor cannot dig a hole in their capital. Preserving capital, limiting loss, and having a disciplined money management approach are some of the keys to successful investing and trading.

Tuesday, December 7, 2010

Mr. Carl Icahn Lecture

Mr. Carl Icahn made his fortune buying undervalued companies that were poorly managed. One can feel pretty pessimistic listening to his lecture in Mr. Robert Shiller’s class at Yale. He stresses that America cannot compete because many companies are undermanaged. He also believes there is no accountability or corporate democracy in America. Interestingly, he admits he is not a manager, but instead puts managers in place who change the structure of the companies he invests in.

Some other topics he discusses are that America is overleveraged, it is very questionable Americans will be able to pay back their debts, and the housing crisis is a mess. In addition, he still believes making a career on Wall Street is a good choice.

Some of his positive influences in life are Aristotle’s Nicomachean Ethics and Rudyard Kipling’s poem IF. He mentioned that he reads IF from time to time. Mr. Icahn also suggests to the students to not be overconfident in their abilities when times are going well, and to not get too down when things are not going well. In addition, he suggests that by working hard and having faith in your abilities is a good way to be in life.

When asked about poor corporate governance in America Mr. Icahn mentioned that Canada and England have better models. He also felt that poison pills and staggered boards are some examples of how companies protect themselves and entrench their managements.

I really did not learn very much from his lecture, perhaps because I am familiar with his past. I am, however, interested in reading Aristotle and will turn to that at some point in the near future.

Some other topics he discusses are that America is overleveraged, it is very questionable Americans will be able to pay back their debts, and the housing crisis is a mess. In addition, he still believes making a career on Wall Street is a good choice.

Some of his positive influences in life are Aristotle’s Nicomachean Ethics and Rudyard Kipling’s poem IF. He mentioned that he reads IF from time to time. Mr. Icahn also suggests to the students to not be overconfident in their abilities when times are going well, and to not get too down when things are not going well. In addition, he suggests that by working hard and having faith in your abilities is a good way to be in life.

When asked about poor corporate governance in America Mr. Icahn mentioned that Canada and England have better models. He also felt that poison pills and staggered boards are some examples of how companies protect themselves and entrench their managements.

I really did not learn very much from his lecture, perhaps because I am familiar with his past. I am, however, interested in reading Aristotle and will turn to that at some point in the near future.

Monday, December 6, 2010

Drawdowns in Sports

I was watching the Indianapolis Colts against the Dallas Cowboys yesterday. It was a fun game to watch. Although I am not a fan of either team, it was painful to watch Mr. Peyton Manning. He is in one of the worst slumps of his career. Mr. Manning has thrown 11 interceptions in his last three games. His former coach mentioned that he has not seen him do this poorly since the early 2000’s.

I realized that what I was watching was a man in drawdown. It occurs to everyone. Bad cycles and times are a part of sports, trading, and life. Mr. Manning is a future Hall of Fame quarterback. At some point he will come out of this as he came out of it in the early 2000’s. The lesson for all of us is to persevere and work right through these negative periods.

I realized that what I was watching was a man in drawdown. It occurs to everyone. Bad cycles and times are a part of sports, trading, and life. Mr. Manning is a future Hall of Fame quarterback. At some point he will come out of this as he came out of it in the early 2000’s. The lesson for all of us is to persevere and work right through these negative periods.

Saturday, December 4, 2010

From zzjoke.com

Sherlock Holmes and Dr Watson go on a camping trip. After a good dinner and a bottle of wine, they retire for the night, and go to sleep.

Some hours later, Holmes wakes up and nudges his faithful friend. "Watson, look up at the sky and tell me what you see."

"I see millions and millions of stars, Holmes" replies Watson.

"And what do you deduce from that?"

Watson ponders for a minute.

"Well, astronomically, it tells me that there are millions of galaxies and potentially billions of planets. Astrologically, I observe that Saturn is in Leo. Horologically, I deduce that the time is approximately a quarter past three. Meteorologically, I suspect that we will have a beautiful day tomorrow. Theologically, I can see that God is all powerful, and that we are a small and insignificant part of the universe. What does it tell you, Holmes?"

Holmes is silent for a moment. "Watson, you idiot!" he says. "Someone has stolen our tent!"

Some hours later, Holmes wakes up and nudges his faithful friend. "Watson, look up at the sky and tell me what you see."

"I see millions and millions of stars, Holmes" replies Watson.

"And what do you deduce from that?"

Watson ponders for a minute.

"Well, astronomically, it tells me that there are millions of galaxies and potentially billions of planets. Astrologically, I observe that Saturn is in Leo. Horologically, I deduce that the time is approximately a quarter past three. Meteorologically, I suspect that we will have a beautiful day tomorrow. Theologically, I can see that God is all powerful, and that we are a small and insignificant part of the universe. What does it tell you, Holmes?"

Holmes is silent for a moment. "Watson, you idiot!" he says. "Someone has stolen our tent!"

Friday, December 3, 2010

Wealth, War and Wisdom - Mr. Barton Biggs

I have recently read Wealth, War and Wisdom by Mr. Barton Biggs. This book was an enjoyable read and I learned more about World War II and how markets reacted during the period from the Great Crash of 1929 until approximately 1945.

The main thesis of the book is that there is wisdom in crowd behavior as exhibited by market prices. Although the markets may misprice assets and bubbles do occur, Mr. Biggs states that the markets correctly predicted the future at major turning points in WWII. In particular, Mr. Biggs states that markets bottomed and turned during the Battle of Britain and The Battle of Midway and peaked in Germany when they attacked Russia.

Mr. Biggs makes the case that real returns in stocks far surpassed returns in bills and bonds for all countries. In particular, real returns from stocks in the countries that were “lucky,” generally the ones who won the war and were not occupied, also surpassed the real returns from stocks in the countries which were unlucky, generally the losers of WWII and those that had been occupied by the Axis powers.

There is also good advice for wealthy people and what they should do in times of crises and war; however, I am not going to go into this here. In addition, Mr. Biggs also observes how black marketeers became wealthy in all the wars around the world; that food, warm clothing, and cigarettes became tradable commodities, and easily transportable wealth like jewelry was helpful to have during these times.

The main conclusion of the book is best summarized by Mr. Biggs himself:

“I argue that the stock market, because it is the collective conclusion of multiple, independent, diverse, decentralized, motivated judgements, is a far different creature from the mob or group. This is not to claim that the stock market is all wise or cannot make mistakes or in the short term misjudge events. I am saying that in general its judgement is good and worth paying attention to.”

The main thesis of the book is that there is wisdom in crowd behavior as exhibited by market prices. Although the markets may misprice assets and bubbles do occur, Mr. Biggs states that the markets correctly predicted the future at major turning points in WWII. In particular, Mr. Biggs states that markets bottomed and turned during the Battle of Britain and The Battle of Midway and peaked in Germany when they attacked Russia.

Mr. Biggs makes the case that real returns in stocks far surpassed returns in bills and bonds for all countries. In particular, real returns from stocks in the countries that were “lucky,” generally the ones who won the war and were not occupied, also surpassed the real returns from stocks in the countries which were unlucky, generally the losers of WWII and those that had been occupied by the Axis powers.

There is also good advice for wealthy people and what they should do in times of crises and war; however, I am not going to go into this here. In addition, Mr. Biggs also observes how black marketeers became wealthy in all the wars around the world; that food, warm clothing, and cigarettes became tradable commodities, and easily transportable wealth like jewelry was helpful to have during these times.

The main conclusion of the book is best summarized by Mr. Biggs himself:

“I argue that the stock market, because it is the collective conclusion of multiple, independent, diverse, decentralized, motivated judgements, is a far different creature from the mob or group. This is not to claim that the stock market is all wise or cannot make mistakes or in the short term misjudge events. I am saying that in general its judgement is good and worth paying attention to.”

Thursday, December 2, 2010

Winston Churchill's Big Black Dog - Biggs - Trading

In Mr. Biggs book, Hedgehogging, he discusses the periodic bouts of depression that Winston Churchill would have.

“Winston Churchill, whose career had its ups and downs and also was plagued with bouts of depression, spoke of the huge, foul-smelling black dog with breath like the sewer, which appeared uninvited and sat heavily on his chest, pinning him down.”

Well, in all my years of trading, I can empathize with Mr. Churchill. That big, black dog is now visiting me and sitting on my chest.

All professional money managers and traders understand that there will be times when they underperform. Mr. Buffett, I believe, said that it can be up to 30% of the time that managers underperform. Mr. Biggs discusses the frustration money managers have with their investors when they do not perform well. As soon as a fund does not perform well, investors usually take the money and run, instead of waiting and being patient. Investors immediately begin to search for someone else who can make them money.

Generally, the good money manager is one who performs well, on average, over a long time frame. Mr. Biggs argues that investors would probably be better off staying with a manager with a proven long term record, rather than going out and searching for superstars and returns, just because of a bad year.

Just some food for thought…

“Winston Churchill, whose career had its ups and downs and also was plagued with bouts of depression, spoke of the huge, foul-smelling black dog with breath like the sewer, which appeared uninvited and sat heavily on his chest, pinning him down.”

Well, in all my years of trading, I can empathize with Mr. Churchill. That big, black dog is now visiting me and sitting on my chest.

All professional money managers and traders understand that there will be times when they underperform. Mr. Buffett, I believe, said that it can be up to 30% of the time that managers underperform. Mr. Biggs discusses the frustration money managers have with their investors when they do not perform well. As soon as a fund does not perform well, investors usually take the money and run, instead of waiting and being patient. Investors immediately begin to search for someone else who can make them money.

Generally, the good money manager is one who performs well, on average, over a long time frame. Mr. Biggs argues that investors would probably be better off staying with a manager with a proven long term record, rather than going out and searching for superstars and returns, just because of a bad year.

Just some food for thought…

Wednesday, December 1, 2010

Emini Trading Performance for 2010

Our trading for 2010 is now completed (we do not trade in December). Our performance for 2010 was disappointing and frustrating. Tradingxyz’s point losses for 2010 were 2.50 points. Depending on the risk level chosen, this would have been:

1% risk = -.5%

2% risk = -1.1%

3.5% risk = -2.5%

This was our first losing year relative to our historical performance. Although the losses were relatively small, they were painful. It is always painful to lose money. In trading it is well known that losses are much more painful and memorable than gains. It is even more painful to underperform, but we will withhold judgement on this until the end of the year, when our performance benchmarks will be computed.

Nonetheless, one of the main aspects of money management and risk control is to not get blown out of the water. Good trading is about preserving capital and having it available in order to capture future opportunities. Our historical performance has been excellent and will return. The loss for 2010 was small, and generally insignificant, when one has a longer term perspective. Our capital has been preserved and we look forward to a much better year of trading in 2011.

1% risk = -.5%

2% risk = -1.1%

3.5% risk = -2.5%

This was our first losing year relative to our historical performance. Although the losses were relatively small, they were painful. It is always painful to lose money. In trading it is well known that losses are much more painful and memorable than gains. It is even more painful to underperform, but we will withhold judgement on this until the end of the year, when our performance benchmarks will be computed.

Nonetheless, one of the main aspects of money management and risk control is to not get blown out of the water. Good trading is about preserving capital and having it available in order to capture future opportunities. Our historical performance has been excellent and will return. The loss for 2010 was small, and generally insignificant, when one has a longer term perspective. Our capital has been preserved and we look forward to a much better year of trading in 2011.

Tuesday, November 30, 2010

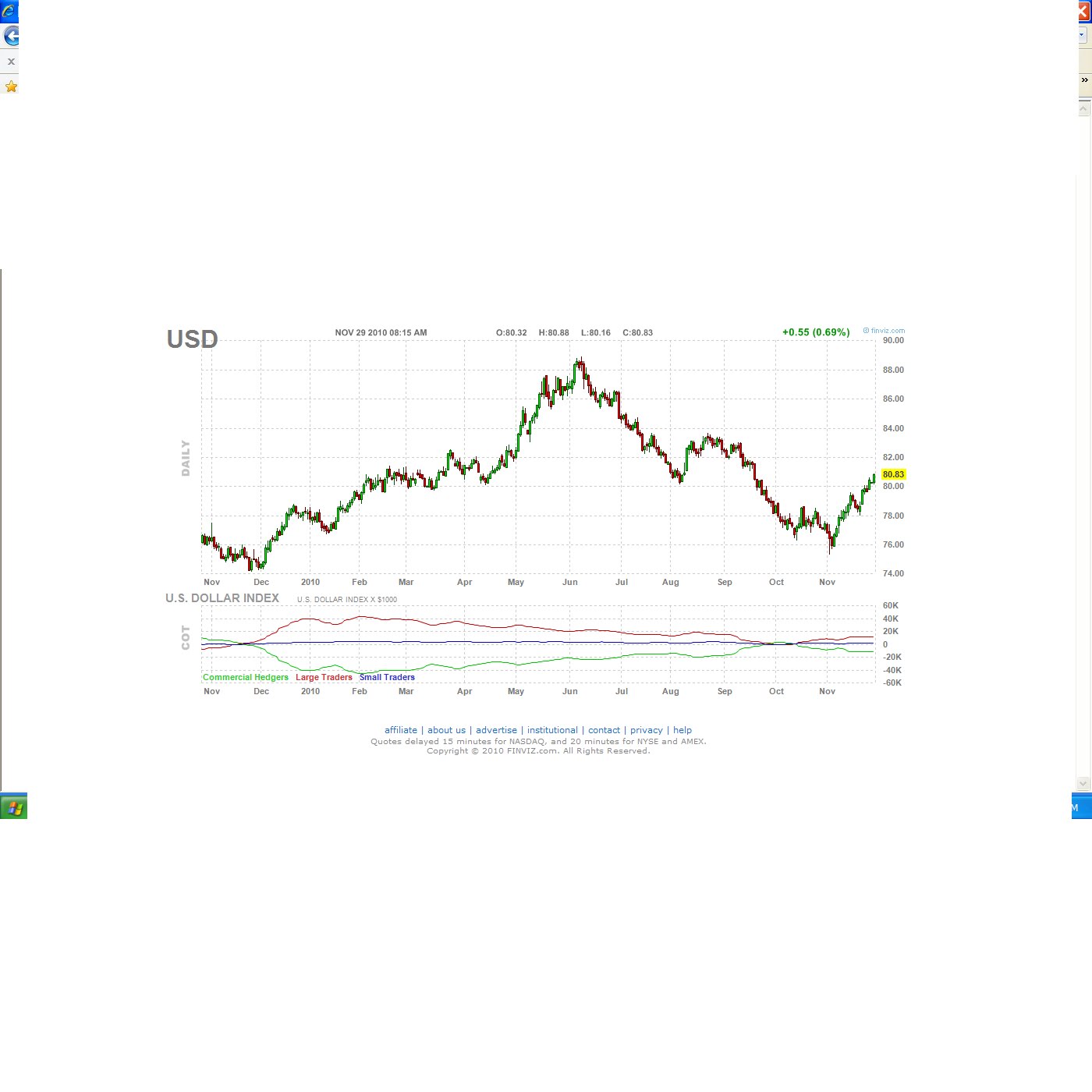

Is QE2 Failing?

All the reasons for the Fed’s QE2 program have now been explained; they are trying to lower the value of the US dollar, lower long term interest rates, and that they are trying to avoid deflation. A quick look at the US dollar and 30 year bond charts, since early November, show that exactly the opposite is happening.

The US dollar has appreciated and bond prices have gone down; yields have gone up. Does this mean that the program is not having its intended effects? Or does it mean that the markets already anticipated the Fed’s move and moved before the Fed announcement? I know it may be early, but so far, so bad.

I also would not rule out that other countries, particularly China, may be behind this. China has been vocal and has stated that they are not happy with the Fed’s program. Maybe China is dumping some of its bond holdings and buying dollars? Who knows? …but I would not rule this out as a possibility. China has been recently flexing its economic muscle and they have even downgraded US bond credit ratings, so it’s not impossible that they are moving to counter the Fed’s actions.

Monday, November 29, 2010

Mr. Joseph Campbell - Taking the Left Hand Path and Traders

The other day I was watching some lectures given by Mr. Joseph Campbell. Mr. Campbell was known for his interdisciplinary studies in mythology. In his lecture he mentioned taking the “left-hand path” in life. There are many definitions and ideas associated with the left, and the left-hand path, however, in this particular lecture Mr. Campbell was discussing the hero’s journey.

The mythological hero who takes the left hand path is taking the unconventional, not tried, and risky path. The person who follows the right hand path can be considered risk averse, conventional, and comfortable following the herd. The hero who takes the left hand path must be confident, understand that he or she may or may not be helped along the way, and if they return unharmed will be stronger going forward. The strength gained may be emotional, psychological, or physical.

Nonetheless, this all made me think about traders. Traders to me are people who follow the left hand path in life. They deal with risks everyday. The way they trade and their choice of working for money in this way is unconventional. The trader faces difficulties and pressure under stressful market conditions, which are similar to the trial a hero may face. It is during the trial that the hero will succeed. Are you following the left-hand path in life? For those who do, the rewards are enormous.

The mythological hero who takes the left hand path is taking the unconventional, not tried, and risky path. The person who follows the right hand path can be considered risk averse, conventional, and comfortable following the herd. The hero who takes the left hand path must be confident, understand that he or she may or may not be helped along the way, and if they return unharmed will be stronger going forward. The strength gained may be emotional, psychological, or physical.

Nonetheless, this all made me think about traders. Traders to me are people who follow the left hand path in life. They deal with risks everyday. The way they trade and their choice of working for money in this way is unconventional. The trader faces difficulties and pressure under stressful market conditions, which are similar to the trial a hero may face. It is during the trial that the hero will succeed. Are you following the left-hand path in life? For those who do, the rewards are enormous.

Saturday, November 27, 2010

Smile and be Thankful...

A guy calls up his stock broker’s office and asks to speak to his broker Mr. Smith. After an awkward pause the receptionist at the other end informs the client that his broker had died. The caller says nothing in response and hangs up the phone.

A while later the client calls up the office again and asks to speak to his broker. The receptionist pauses for a moment and responds by saying "I'm sorry sir, but your broker is dead." Again, the man says nothing and hangs up the phone.

Several hours later the man calls up again making the same request. The bewildered receptionist asks the caller "Haven't you called here already today asking to speak to Mr. Smith?" The caller replies with a simple "No." The receptionist once again informs the gentleman that his broker has died.

Later on that day the same client calls up the office again, asking to speak to his broker. This time the receptionist is certain that it’s the same guy calling again, so she transfers him to the manager. The manager picks up the phone and offers his assistance. After the caller requests to speak to his broker, the manager responds, "Sir, we have records that you have already called here three times today. Each time you ask to speak to your broker and each time we inform you that your broker has passed away. Why do you keep calling? Don't you realize that the man is dead?"

To this the caller responds, "Oh, I realize that he's dead, I just like to hear you say it..."

A while later the client calls up the office again and asks to speak to his broker. The receptionist pauses for a moment and responds by saying "I'm sorry sir, but your broker is dead." Again, the man says nothing and hangs up the phone.

Several hours later the man calls up again making the same request. The bewildered receptionist asks the caller "Haven't you called here already today asking to speak to Mr. Smith?" The caller replies with a simple "No." The receptionist once again informs the gentleman that his broker has died.

Later on that day the same client calls up the office again, asking to speak to his broker. This time the receptionist is certain that it’s the same guy calling again, so she transfers him to the manager. The manager picks up the phone and offers his assistance. After the caller requests to speak to his broker, the manager responds, "Sir, we have records that you have already called here three times today. Each time you ask to speak to your broker and each time we inform you that your broker has passed away. Why do you keep calling? Don't you realize that the man is dead?"

To this the caller responds, "Oh, I realize that he's dead, I just like to hear you say it..."

Tuesday, November 23, 2010

Mr. Andrew Redleaf Lecture

Recently I have been watching videos on Youtube of guest lecturers in Mr. Robert Shiller’s class at Yale. I have recently watched Mr. Andrew Redleaf. What a great source of information these videos are. I encourage you to go into Youtube and search for Yale’s videos.

Mr. Redleaf runs a hedge fund. His lecture centered mostly on efficient markets, the two types of investors that exist, and how he runs his shop. Mr. Redleaf does not believe in the efficiency of markets and describes examples where mispricing and inefficiencies seem to appear; for example, when closed-end funds trade at a discount or premium to the assets they hold, or if a company owns shares in a different company but the value of those shares is not reflected in the stock. One example he gave was when 3Com owned Palm shares.

Mr. Redleaf’s lecture was interesting, but not riveting. What I did like about it and some of the points that interested me were the following:

There are generally two kinds of investors: coupon clippers and security resellers. A coupon clipper is someone who generally analyzes investments from a cash flow perspective. Similar to how bond holders would redeem their coupons and receive the cash flow or interest from their bond holdings. He mentions that Mr. Buffett is a coupon clipper and how Mr. Buffett tends to look for the coupon in equities. Security resellers, on the other hand, are those who buy something and look to resell it at a higher price.

Mr. Redleaf also described the three main concepts his firm uses. The first is that they are coupon clippers. What kind of coupons can we extract is a general philosophy of his. The second is analyzing risk. What’s the worst thing that can go wrong? (By the way he thinks VAR analysis is fundamentally wrong). And lastly, how do we eliminate the risks that we have? He provides an example of these concepts of how his firm may own a high-yield bond and short the stock of the company as a hedge.

I thought the best point made in his lecture was that he likes to think that firms or people get paid to eliminate risk, not for taking it. Overall, I learned something and thought it was interesting. If you have the time, watch it, if not, I think I just outlined his main points.

Mr. Redleaf runs a hedge fund. His lecture centered mostly on efficient markets, the two types of investors that exist, and how he runs his shop. Mr. Redleaf does not believe in the efficiency of markets and describes examples where mispricing and inefficiencies seem to appear; for example, when closed-end funds trade at a discount or premium to the assets they hold, or if a company owns shares in a different company but the value of those shares is not reflected in the stock. One example he gave was when 3Com owned Palm shares.

Mr. Redleaf’s lecture was interesting, but not riveting. What I did like about it and some of the points that interested me were the following:

There are generally two kinds of investors: coupon clippers and security resellers. A coupon clipper is someone who generally analyzes investments from a cash flow perspective. Similar to how bond holders would redeem their coupons and receive the cash flow or interest from their bond holdings. He mentions that Mr. Buffett is a coupon clipper and how Mr. Buffett tends to look for the coupon in equities. Security resellers, on the other hand, are those who buy something and look to resell it at a higher price.

Mr. Redleaf also described the three main concepts his firm uses. The first is that they are coupon clippers. What kind of coupons can we extract is a general philosophy of his. The second is analyzing risk. What’s the worst thing that can go wrong? (By the way he thinks VAR analysis is fundamentally wrong). And lastly, how do we eliminate the risks that we have? He provides an example of these concepts of how his firm may own a high-yield bond and short the stock of the company as a hedge.

I thought the best point made in his lecture was that he likes to think that firms or people get paid to eliminate risk, not for taking it. Overall, I learned something and thought it was interesting. If you have the time, watch it, if not, I think I just outlined his main points.

Saturday, November 20, 2010

Emini Trading System this week

Two trades were taken this week; an X buy and a Y sell, for 1.25 and 1.00 points.

Friday, November 19, 2010

Mr. Aaron Brown - The Poker Face of Wall Street

I have recently finished reading Mr. Aaron Brown’s book, The Poker Face of Wall Street. I have some mixed emotions about this book. I really liked the economic ideas he presented, but I did not care much for the poker parts. This is because I personally am not interested in poker. However, for those who are interested in poker, I think these parts would be of interest to you. Nonetheless, I did want to read the book, and in the end I am glad I did. I have also added it to my recommended reading list.

I think it would have been better if Mr. Brown separated the subjects of poker and finance into two books. I can understand the relationships between finance and gambling, but I was more interested in his insights on economic history and theory. I enjoyed learning about John Law and Fischer Black’s ideas. I found the section on expected value and utility value interesting. And I can also buy into his thesis that risk and gambling lead to capital concentration and further reinvestment. He did a nice job in all the subjects he discussed. I feel I now have a better understanding of why gambling is important for a society and its economy.

Lastly, Mr. Brown adds detailed references and recommendations of many other books at the end of his book. A good book, in my opinion, stimulates learning and ideas. Mr. Brown’s book did this for me, and I will be reading some of his recommended books in the near future.

I think it would have been better if Mr. Brown separated the subjects of poker and finance into two books. I can understand the relationships between finance and gambling, but I was more interested in his insights on economic history and theory. I enjoyed learning about John Law and Fischer Black’s ideas. I found the section on expected value and utility value interesting. And I can also buy into his thesis that risk and gambling lead to capital concentration and further reinvestment. He did a nice job in all the subjects he discussed. I feel I now have a better understanding of why gambling is important for a society and its economy.

Lastly, Mr. Brown adds detailed references and recommendations of many other books at the end of his book. A good book, in my opinion, stimulates learning and ideas. Mr. Brown’s book did this for me, and I will be reading some of his recommended books in the near future.

Thursday, November 18, 2010

Mr. Barton Biggs and Hedgehogging

Mr. Barton Biggs has written a book called, Hedgehogging. Mr. Biggs used to be the head of Morgan Stanley’s Asset Management business and research groups. He now works for himself at his hedge fund called Traxis Partners LP.

In my opinion, this is not a very catchy title for a book, nonetheless, it really is a very good book to read. When I was younger I worked for a small firm that had close ties to Morgan Stanley and we used the firm for its trading and research. I used to read many research reports, but I remember always wanting to read his research reports and letters to clients.

The book is not a how-to type of book. It is a collection of many stories and ideas that he has gathered over a lifetime of investing. His varied investment experiences and broad thoughts on many topics make the book fun to read and very thought-provoking. I highly recommend it and I am putting in my recommended reading list. I will also be writing about some of the concepts discussed in the book in the near future. Now it’s onto Mr. Soros’ latest book, The Credit Crises of 2008 and What It Means.

In my opinion, this is not a very catchy title for a book, nonetheless, it really is a very good book to read. When I was younger I worked for a small firm that had close ties to Morgan Stanley and we used the firm for its trading and research. I used to read many research reports, but I remember always wanting to read his research reports and letters to clients.

The book is not a how-to type of book. It is a collection of many stories and ideas that he has gathered over a lifetime of investing. His varied investment experiences and broad thoughts on many topics make the book fun to read and very thought-provoking. I highly recommend it and I am putting in my recommended reading list. I will also be writing about some of the concepts discussed in the book in the near future. Now it’s onto Mr. Soros’ latest book, The Credit Crises of 2008 and What It Means.

Tuesday, November 16, 2010

Why Beauty is Important in Trading Systems and Trading Models – Emini Trading System

In Mr. Arthur Koestler’s book, The Act of Creation, he relates a story that occurred between Mr. Erwin Schrödinger and Mr. Paul Dirac, two founders of quantum mechanic who shared a Nobel Prize in 1933. Mr. Dirac tells a story of how Mr. Schrödinger created his wave equation of the electron. Mr. Schrödinger concentrated on developing his ideas by relying on his thoughts and by making beautiful generalizations, rather than relying closely on experimental data. Mr. Dirac states,

“I think there is a moral to this story, namely that it is more important to have beauty in one’s equations than to have them fit experiment. If Schrödinger had been more confident of his work, he could have published it some months earlier, and he could have published a more accurate equation…It seems that if one is working from the point of view of getting beauty in one’s equations, and if one really has a sound insight, one is on a sure line of progress. If there is not complete agreement between the results of one’s work and experiment, one should not allow oneself to be too discouraged, because the discrepancy may well be due to minor features that are not properly taken into account and that will get cleared up with further developments of the theory...”

I think the moral of this story is that as we develop our trading models and trading systems we too should consider beauty. Are our trading models and systems “beautiful”? Or are they a jumble and a mess of ideas? Mathematicians look at equations and theories and can see beauty in them. All type of art forms have beauty in them. As trading system creators, we too should not forget to make our models “beautiful.”

“I think there is a moral to this story, namely that it is more important to have beauty in one’s equations than to have them fit experiment. If Schrödinger had been more confident of his work, he could have published it some months earlier, and he could have published a more accurate equation…It seems that if one is working from the point of view of getting beauty in one’s equations, and if one really has a sound insight, one is on a sure line of progress. If there is not complete agreement between the results of one’s work and experiment, one should not allow oneself to be too discouraged, because the discrepancy may well be due to minor features that are not properly taken into account and that will get cleared up with further developments of the theory...”

I think the moral of this story is that as we develop our trading models and trading systems we too should consider beauty. Are our trading models and systems “beautiful”? Or are they a jumble and a mess of ideas? Mathematicians look at equations and theories and can see beauty in them. All type of art forms have beauty in them. As trading system creators, we too should not forget to make our models “beautiful.”

Joke

A drunk was proudly showing off his new apartment to a couple of his friends late one night, and led the way to his bedroom where there was a big brass gong.

"What's that big brass gong?" one of the guests asked.

"It's not a gong. It's a talking clock," the drunk replied.

"A talking clock? Seriously?" asked his astonished friend.

"Yup," replied the drunk.

"How's it work?" the friend asked, squinting at it.

"Watch," the drunk replied. He picked up the mallet, gave it an ear-shattering pound, and stepped back. The three stood looking at one another for a moment.

Suddenly, someone on the other side of the wall screamed, "You bastard it's ten past three in the morning!"

-from my friend at ZZJoke.com

"What's that big brass gong?" one of the guests asked.

"It's not a gong. It's a talking clock," the drunk replied.

"A talking clock? Seriously?" asked his astonished friend.

"Yup," replied the drunk.

"How's it work?" the friend asked, squinting at it.

"Watch," the drunk replied. He picked up the mallet, gave it an ear-shattering pound, and stepped back. The three stood looking at one another for a moment.

Suddenly, someone on the other side of the wall screamed, "You bastard it's ten past three in the morning!"

-from my friend at ZZJoke.com

Monday, November 15, 2010

Mr. Jeremy Grantham's 3Q 2010 Letter

For those of you who are stock investors, reading and utilizing Mr. Grantham's advice may be helpful. I really enjoyed reading this letter.

Sunday, November 14, 2010

Friday, November 12, 2010

Mr. Jeremy Grantham's Warning and Advice

Mr. Jeremy Grantham, a partner in the asset management firm Grantham, Mayo, Van Otterloo, was recently interviewed on CNBC. Mr. Grantham has criticized the Fed's actions; both under Mr. Greenspan and Mr. Bernanke. As a professional analyst of bubbles, Mr. Grantham makes the case that the Fed is basically leading us to the next disaster. He feels that both the bond and stock markets are overvalued. Holding cash and being patient will provide options and the opportunity to invest when these market bubbles collapse. His opinion of fair value in the SP500 is around 900. This interview is well worth watching.

Tuesday, November 9, 2010

Mr. Aaron Brown - The Poker Face of Wall Street

Yesterday I began to read this book. I am not a poker player but I am interested to see how he ties the game of poker to finance.

Maybe I'll also learn to how to break Vegas and AC...:)

Maybe I'll also learn to how to break Vegas and AC...:)

Monday, November 8, 2010

Mr. Emanuel Derman - My Life as a Quant: Reflections on Physics and Finance

I have just completed reading Mr. Derman's book. I really liked it and would recommend it to anyone interested in modeling, quantitative finance, or financial engineering. I will also be adding it to my recommended reading list.

I will be writing more about this book in the near future.

I will be writing more about this book in the near future.

Saturday, November 6, 2010

Emini System Trading This Week

No trades this week.

Meanwhile here is some humor from ZZJoke.com

There is a new study out about women and how they feel about their ass:

85% of women think their ass is too big...

10% of women think their ass is too little...

The other 5% say that they don't care - they love him and would have married him anyway!!

Meanwhile here is some humor from ZZJoke.com

There is a new study out about women and how they feel about their ass:

85% of women think their ass is too big...

10% of women think their ass is too little...

The other 5% say that they don't care - they love him and would have married him anyway!!

Friday, November 5, 2010

Working through Underperformance as a System Trader

This is a quote by Eleanor Roosevelt which I would like to share with you. I find it inspiring and helpful.

“The future belongs to those who believe in the beauty of their dreams.”

When times are tough and you are underperforming, especially as a system trader, you need to stay optimistic and know that you will experience good and bad times. It is just the nature of the game. We now have three trading weeks left before we close out the year. I am interested to see how things play out.

Looking at our historical data we know that rough years can occur. This year has been one of them, as was 2002. My models and my heart also tell me that when I look at the historical results, I also see great performance the years following a relatively poor year. Let’s see what happens…

“The future belongs to those who believe in the beauty of their dreams.”

When times are tough and you are underperforming, especially as a system trader, you need to stay optimistic and know that you will experience good and bad times. It is just the nature of the game. We now have three trading weeks left before we close out the year. I am interested to see how things play out.

Looking at our historical data we know that rough years can occur. This year has been one of them, as was 2002. My models and my heart also tell me that when I look at the historical results, I also see great performance the years following a relatively poor year. Let’s see what happens…

Thursday, November 4, 2010

Mr. Lewis Borsellino and Mr. Robert Shiller - Irrational Exuberance

I have been reading financial books lately. I have now finished Mr. Lewis Borsellino’s book, The Day Trader: From the Pit to the PC. I have also finished reading Irrational Exuberance, by Mr. Robert J. Shiller. It takes a lot, in my own mind of course, to make it into my reading list. Mr. Borsellino’s book does not make the cut because it produced very few, if any, good ideas for me. In other words, it did not make me think much. One criterion of a good book is that it should make one think.

Mr. Shiller’s book, on the other hand, does score a few points on the thinking front. Although the book was quite boring in some parts, I did find it interesting to read. I would recommend it, but I am not going to put it in my reading list. I will, however, be writing about some of the ideas that I thought were important and interesting from Mr. Shiller’s book in the near future.

For now, I would like to go back to Mr. Borsellino’s book and take out, what I thought, was the meat from it. As traders, we instinctively understand this, but it is always good to read things from successful traders who have “been there, and done that.” Here are three quotes from the book:

“Where there is risk, however, there is also fear. Fear cannot be avoided, and it is not a sign of weakness to feel it. The important thing about fear is how to handle it. Mastering fear propels you forward. Letting fear master you paralyzes you.”

“to be successful in life, especially in trading, which puts your money on the line every day, you cannot be a prisoner of your own thoughts.”

In regards to one of the lessons his father taught him, “he gave us stomachs for risk and the ability to push past the fear.”

Good stuff and well worth remembering as a trader and as a human being. What I also like is that he says that fear is not a sign of weakness to feel; it is something to acknowledge, feel, and use.

Mr. Shiller’s book, on the other hand, does score a few points on the thinking front. Although the book was quite boring in some parts, I did find it interesting to read. I would recommend it, but I am not going to put it in my reading list. I will, however, be writing about some of the ideas that I thought were important and interesting from Mr. Shiller’s book in the near future.

For now, I would like to go back to Mr. Borsellino’s book and take out, what I thought, was the meat from it. As traders, we instinctively understand this, but it is always good to read things from successful traders who have “been there, and done that.” Here are three quotes from the book:

“Where there is risk, however, there is also fear. Fear cannot be avoided, and it is not a sign of weakness to feel it. The important thing about fear is how to handle it. Mastering fear propels you forward. Letting fear master you paralyzes you.”

“to be successful in life, especially in trading, which puts your money on the line every day, you cannot be a prisoner of your own thoughts.”

In regards to one of the lessons his father taught him, “he gave us stomachs for risk and the ability to push past the fear.”

Good stuff and well worth remembering as a trader and as a human being. What I also like is that he says that fear is not a sign of weakness to feel; it is something to acknowledge, feel, and use.

Wednesday, November 3, 2010

Mr. Lewis J. Borsellino's Book; The Day Trader:From the Pit to the PC

Mr. Lewis J. Borsellino wrote a book called The Day Trader: From the Pit to the PC. Mr. Borsellino was one of the biggest, if not the biggest traders of the S&P futures contract at the Chicago Merc.

Mr. Borsellino’s book was interesting only if you are interested in his autobiography. He relates many stories about himself and of his father. The book, however, is a disappointment if you are looking for trading insights. Although he tells you how he made zillions on trades, he never describes ideas, insights, or methods on how he did it.

I am always looking for new ideas to explore and test. Mr. Borsellino’s book, like many other trading books out there, will disappoint you if you are looking for trading ideas.

Mr. Borsellino’s book was interesting only if you are interested in his autobiography. He relates many stories about himself and of his father. The book, however, is a disappointment if you are looking for trading insights. Although he tells you how he made zillions on trades, he never describes ideas, insights, or methods on how he did it.

I am always looking for new ideas to explore and test. Mr. Borsellino’s book, like many other trading books out there, will disappoint you if you are looking for trading ideas.

Tuesday, November 2, 2010

The Federal Reserve and Quantitative Easing

The Federal Reserve is expected to announce their new policy of “quantitative easing.”

Q. Does anyone really understand what the Fed is doing?

A. Nope.

Q. Does anyone understand if they should do 100 billion, 500 billion, or 1 trillion dollars in purchases?

A. Nope.

Q. Does anyone understand what the effects of this program will be?

A. Nope.

Q. Does anyone understand if they should include mortgage backed securities, 30 year bonds, CDO’s, and generally any garbage that can be purchased?

A. Nope.

Q. Does Wall Street and the market understand what this will really do for the economy?

A. Nope.

Q. Does the Fed itself know what it is doing?

You guessed it…

Have a nice day:)

Q. Does anyone really understand what the Fed is doing?

A. Nope.

Q. Does anyone understand if they should do 100 billion, 500 billion, or 1 trillion dollars in purchases?

A. Nope.

Q. Does anyone understand what the effects of this program will be?

A. Nope.

Q. Does anyone understand if they should include mortgage backed securities, 30 year bonds, CDO’s, and generally any garbage that can be purchased?

A. Nope.

Q. Does Wall Street and the market understand what this will really do for the economy?

A. Nope.

Q. Does the Fed itself know what it is doing?

You guessed it…

Have a nice day:)

Saturday, October 30, 2010

Friday, October 29, 2010

Greek Debt and Mr. El-Erian

Mr. Mohamed A. El-Erian was recently discussing the Greek debt problem as reported by Bloomberg.com.

He stated that Greece is likely to default on their debt by 2013. Mr. El-Erian felt that, it’s in Greece’s interest to default “as long as you can contain the contagion to other countries and it is done through orderly restructuring and repricing to retain competitiveness.” I definitely agree that it is only a matter of time before the Greeks default, but I have a feeling that it will not be an orderly process. These kinds of things spread like wildfire and can be very difficult to control and keep orderly once they begin to happen.

Mr. El-Erian always seems to be in the news recently. He and Mr. Nouriel Roubini are now officially the twins of doom. I like both of these men, and I am kidding when I say this, but there is some truth to the statement. Mr. El-Erian calls it like he sees it. It is only a matter of time before the overleveraged countries pay for their mistakes. It happens to individuals and it will happen to countries. Greece may be first, but remember, there is line at the door to bankruptcy and default…and it “ain’t going to be purty at all.”

He stated that Greece is likely to default on their debt by 2013. Mr. El-Erian felt that, it’s in Greece’s interest to default “as long as you can contain the contagion to other countries and it is done through orderly restructuring and repricing to retain competitiveness.” I definitely agree that it is only a matter of time before the Greeks default, but I have a feeling that it will not be an orderly process. These kinds of things spread like wildfire and can be very difficult to control and keep orderly once they begin to happen.

Mr. El-Erian always seems to be in the news recently. He and Mr. Nouriel Roubini are now officially the twins of doom. I like both of these men, and I am kidding when I say this, but there is some truth to the statement. Mr. El-Erian calls it like he sees it. It is only a matter of time before the overleveraged countries pay for their mistakes. It happens to individuals and it will happen to countries. Greece may be first, but remember, there is line at the door to bankruptcy and default…and it “ain’t going to be purty at all.”

Wednesday, October 27, 2010

The dilemma of market prices and Information Theory

Can information theory help us better understand market price behavior? Information theory states that an unexpected event or signal that occurs contains more informational content than an event that is expected. I can follow the logic of this. But here is the dilemma; if a signal or an event contains more information, it theoretically should reduce uncertainty.

When the market receives unexpected news, prices immediately react, but the sudden reaction in prices does not generally reduce uncertainty, it increases it. In my opinion, given everything else, if the news has been expected, one should expect market prices to be range bound with negative feedback dominating price moves. But if the news is unexpected, then a price breakout in some direction usually occurs. Price breakouts are positive feedback events that generally create herdlike trading. Although the unexpected news event may contain more information, it does not necessarily lessen uncertainty, it increases it. This can lead to trading opportunities for discretionary style traders.

I have difficulty understanding how discretionary traders can make money on a consistent basis. Discretionary traders not only have to figure out what direction prices are going to move, but they also have to determine if the news is expected or unexpected. This is why we see the market move so much when economic figures or earnings are released that differ from the consensus opinion. Consensus is synonymous with expected. Relating the actual figure to the consensus number is another aspect that a discretionary trader has to take into account. Then, if that is not hard enough, the discretionary trader has to figure how far and in what timeframe prices will move. Is it not better to trade the market systematically? I think so.

When the market receives unexpected news, prices immediately react, but the sudden reaction in prices does not generally reduce uncertainty, it increases it. In my opinion, given everything else, if the news has been expected, one should expect market prices to be range bound with negative feedback dominating price moves. But if the news is unexpected, then a price breakout in some direction usually occurs. Price breakouts are positive feedback events that generally create herdlike trading. Although the unexpected news event may contain more information, it does not necessarily lessen uncertainty, it increases it. This can lead to trading opportunities for discretionary style traders.

I have difficulty understanding how discretionary traders can make money on a consistent basis. Discretionary traders not only have to figure out what direction prices are going to move, but they also have to determine if the news is expected or unexpected. This is why we see the market move so much when economic figures or earnings are released that differ from the consensus opinion. Consensus is synonymous with expected. Relating the actual figure to the consensus number is another aspect that a discretionary trader has to take into account. Then, if that is not hard enough, the discretionary trader has to figure how far and in what timeframe prices will move. Is it not better to trade the market systematically? I think so.

Tuesday, October 26, 2010

Mr. Paul Krugman and British Economic Policy

Mr. Paul Krugman, in his column in The New York Times, criticized the recently adopted policies of the British government. Mr. Krugman argues that cutting deficits during difficult economic times is not good policy. This is an argument that many economists make.